Multifamily bridge loans can be a powerful tool for real estate investors—offering speed, flexibility, and a chance to seize opportunities that traditional financing might miss. But as with any financial product, a bridge loan isn’t one-size-fits-all. The terms can vary widely, and understanding the details can make or break your deal.

Before you commit to a multifamily bridge loan, here are 10 smart questions to ask your lender (and yourself) to ensure you're making a strategic, informed decision.

1. What’s the Purpose of the Loan—and Is a Bridge Loan the Right Fit?

Multifamily bridge loans are designed for short-term needs, such as property acquisition, repositioning, or stabilizing before refinancing. Before moving forward, make sure your situation justifies this type of financing. If you're buying a fully stabilized asset with long-term tenants in place, permanent financing might be a better—and cheaper—option.

2. Who Are the Best Multifamily Bridge Lenders for My Type of Project?

Not all lenders are created equal. Some specialize in value-add projects, others in acquisitions or distressed assets. Ask for a lender’s experience with deals like yours. Are they familiar with your market? Do they understand your investment strategy? The right multifamily bridge lender will not only fund the deal but also help you navigate it.

3. What Are the Loan Terms—And What’s the Real Cost?

Beyond the interest rate, be sure you understand all associated costs: origination fees, extension fees, exit fees, and potential penalties. Bridge loans typically come with higher rates than traditional loans, but the speed and flexibility may outweigh the cost—if the math checks out. Ask for a full breakdown of fees and calculate your total cost of capital.

4. How Long Is the Loan Term—and Can It Be Extended?

Most multifamily bridge loans are short-term, often 12 to 36 months. But projects rarely go exactly as planned. Ask if extensions are available, how they work, and what they cost. You want flexibility without being penalized if the timeline shifts.

5. What’s the Required Loan-to-Cost (LTC) or Loan-to-Value (LTV) Ratio?

Understanding the loan’s structure is critical. Many bridge lenders base the loan amount on LTC, meaning a percentage of the total project cost (purchase + rehab), not just the property value. Know your required equity injection up front so you’re not scrambling to raise capital at the last minute.

6. Are Interest Payments Monthly or Rolled Into the Loan?

Some bridge loans require monthly interest-only payments; others allow interest to accrue or be paid at the end. Each structure affects your cash flow differently. If your project won’t generate revenue immediately (like during a renovation), rolled interest might make more sense.

7. What’s the Draw Schedule for Renovation Funds?

If your deal includes construction or upgrades, ask how and when you can access those funds. Lenders usually release rehab funds in stages, based on completed work. Find out what documentation is required for each draw and how long the process takes—it can impact your contractor’s timeline and overall progress.

8. How Will the Property Be Valued?

In a multifamily bridge loan scenario, lenders often base the loan on "as-is" value or "as-completed" value. If they’re using the latter, they’ll need detailed renovation plans and pro forma financials. Knowing how your property will be appraised helps you set realistic expectations and avoid overleveraging.

9. What’s the Exit Strategy—and Is It Realistic?

Every bridge loan needs a clear exit plan. Will you refinance into permanent debt once the property is stabilized? Are you planning to sell after renovations? Lenders will want to know, and so should you. Be honest about timelines, market conditions, and possible delays. A solid exit strategy is what makes a bridge loan low risk rather than high risk.

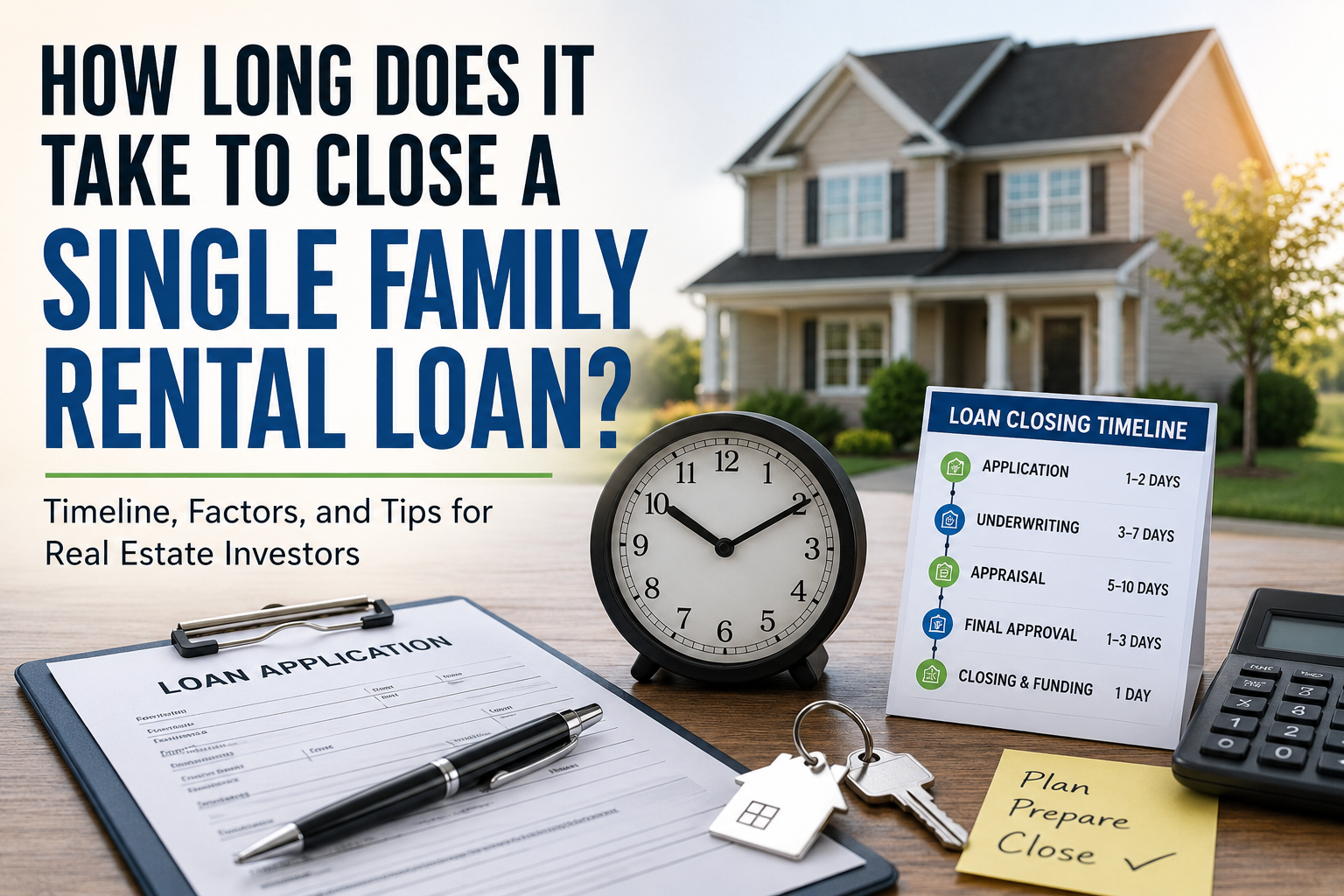

10. How Fast Can You Close?

Speed is one of the main reasons investors turn to bridge financing. In competitive markets, closing fast can mean winning or losing a deal. Ask your lender how quickly they can fund, what documentation they need, and what might delay the process. Great multifamily bridge lenders can close in 10–21 days, assuming you're organized.

Final Thoughts

A multifamily bridge loan can unlock deals and accelerate growth—but only if you understand the terms, risks, and expectations. Rushing into a loan without asking the right questions can lead to costly surprises, strained cash flow, or worse—an unfinished project with no exit.

By pressing your lender for clear, honest answers and reviewing your own plan critically, you’ll be in a far better position to use bridge financing to your advantage. And if you’re looking for experienced multifamily bridge lenders who move fast and think like investors, don’t hesitate to connect with a trusted partner like Simplending Financial.

Write a comment ...